Happy Mid Autumn Festival Guys!

I’ve come to realize that since my investing thesis on Avenue Therapeutics (Avenue Therapeutics – No Pain, Lots Of Gain?), I suddenly have a band of American readers/fellow investors/subscribers.

Apparently, a friend highlighted to me that if you google Avenue Therapeutics, SG TTI’s post on the company is in the 4th link (thereabouts).

Since then, I’ve had a few emails from global readers. This is interesting to me as it’s a fresh and different perspective. Plus I think, most local investors don’t actually understand the thesis that much.

So… to the global readers who would probably not be aware… Mid Autumn Festival is today (13th Sept 2019) and this is a festival whereby folks like myself eat mooncakes and drink tea and supposedly, have to admire the full moon.

Well, skip the full moon part. But I do enjoy mooncakes. They’re absolutely delicious. If you haven’t tried them before, you should.

But try the SG version ones.

I’ve a buddy who’s mainland Chinese (富二代la), and this year, he sent me a box of mooncakes all the way from Beijing. I’ve gotta say, they taste….. weird. It’s just… too different for my liking.

It’s been over a month since my last post:

TTI’s Portfolio Updates – End July 2019 + The Thanos Of Global Macro Funds Is Coming Back!

So let me start with the usual portfolio performance updates.

SG Markets

Total portfolio value in SG markets is SGD 259,582.

Thus far in 2019 (and we’re already 3/4 of the way through the year), I’ve had zero additions in SG, and instead, fully executed on my plan to pare down stakes, take profit or recognize losses in certain holdings and my current SG holdings are a mere fraction of the overall portfolio. Nothing much has changed, and I intend to continue either holding or paring down stakes if the opportunity arises.

Bonds

Nothing much to talk about here, the bond portfolio is approximately SGD 550,000. It’d be another 1-2 yrs before the fruits ripen here. I’ve already mentally locked away this capital.

US / Global Markets

This is where I’ve focused much of my energy and attention on.

Having endured a somewhat rough July & August, the past couple of weeks has been absolutely sweet.

Stats from Interactive Brokers:

US/Global Portfolio NAV has grown to USD 1,068,901.11

But check out the blue line above!

It’s *almost vertical in the past 2 weeks!

Of course, global markets have been really on a tear in the past several weeks, but TTI’s gains have far outstripped the indices in the past fortnight.

This can be attributed to sizable gains in a few larger, core positions such as Centurylink (CTL), Broadcom (AVGO), Chesapeake Energy (CHK) & a significant drop in Beyond Meat (BYND), in which, I have a fairly large short position in the form of naked calls sold.

I’ve also built up a core, 6 digits worth of exposure to HK listed Future Land (1030), that has finally started moving. (In the desired direction of course!).

I put in an estimate in IN, and briefly wrote my thoughts then:

Assuming USD-SGD of 1.37280, overall portfolio NAV is thus now SGD 2,276,969.

US/Global portfolio has returned 36.75% YTD, which is a significant bump up from my last update (TTI’s Portfolio Updates – End July 2019 + The Thanos Of Global Macro Funds Is Coming Back!) of 28.07%

My approach has always been pretty much bottom-up, company specific.

Yet, once in a while, I try to take a step back and look at the big picture, just to have a sense of where we are currently.

And lo and behold…… having done so recently, I find it pretty amazing that despite everything in the news, Trump’s resolve to single handedly upend decades of conventional trading conditions, all the talk of China’s shadow banking debt, the Hong Kong unrest, and even the now, almost sidelined poor Kim and his nukes, the S&P 500 is actually sitting right now, just a tad below it’s all time highs!

I mean, really, check this out. This is what S&P index looks like YTD:

That’s a freaking 20.31% return YTD!

This means that if you’re sitting on say, 18% returns currently, it’d be a winner in most years, but in 2019, it’d be considered a pretty poor performance.

I think a lot of local SG investors fail to consider this.

Really.

Most don’t.

Maybe cos it’s painful to admit that a simple, idiot proof S&P index like SPY is whacking you.

But there’s also a pretty solid argument for using the perennially underperforming STI ETF as a benchmark instead. If you’re an average retail investor, you’d feel more comfortable staying in SG shores, no forex risks, easier to understand the companies, no geographic risk etc. Sure. I get that.

US/Global exchanges are also where many landmines exist IMO. I watched happily as CHK rose almost 20% in a single night sometime last week… but there were days where it fell like 10%++ in a single night as well. It’s stuff that just doesn’t happen in SGX, at least not for a non-penny stock.

If the YTD chart didn’t look impressive enough, check out how it looks like when we zoom out:

After all’s been said and done, we are really still snapping at the all time highs. It’s pretty amazing.

The flood of monies entering passive instruments like SPY (S&P 500 ETF that I use as a benchmark now. I’m trying to mix it up with the big boys eh.), does mean that we have to be cautious here. Michael Burry recently proclaimed that there’s now a bubble in these passive instruments. How so?

Basically some of the smaller constituents of the ETF may have low liquidity, without much investor attention to these companies. Because of the wide spreads, you can also sometimes see large price volatility.

Yet, because of the flood of monies into passive instruments, these low liquidity companies that by themselves, account for a tiny proportion of the index itself, are now suddenly accounting for the fortunes of a large amount of liquidity.

It’s kinda like a leveraging up process. Suddenly now, any volatility in these small constituents, may end up affecting the value (I say value, but it’s really just the prices), of these ETFs that’s tagged to this index.

Yet, this can go on and on and on and on for god knows how long. Personally, I suspect we are along way from this bubble bursting, i.e. there’s much more inflating to go. Simply cos, there are actually people talking about passive instruments as a bubble. We need to wait till it gets so crazy that folks like u and me, are tempted to throw everything into SPY.

That’s when it bursts.

LOL.

Which leads me to another bubble that’s probably going to burst sooner.

BEYOND MEAT.

Now, as the title suggests, I really wanted to write up my investing thesis. But got carried away at the start of this post, and anyway, I’ve come to realize that I don’t really need to impress on anybody why BYND is a bubble.

Everybody seems to know it!

There are already tons of esteemed authors writing about BYND and how it’s way overvalued. Check these out. I’ve read and re-read all of these, but some are now locked up so you can only see the titles, and some snippets. (The comments are fun to read though, and some of these guys are really witty!)

https://seekingalpha.com/article/4288925-beyond-meat-expensive

https://seekingalpha.com/article/4283932-beyond-meat-dramatically-overvalued

https://seekingalpha.com/article/4283512-opinion-beyond-meat-tilray-tale-2-bubbles

https://seekingalpha.com/article/4282108-targeting-36-percent-return-betting-beyond-meat

https://seekingalpha.com/article/4275006-beyond-meat-reductio-ad-absurdum-valuation

AND MANY MORE…

At this stage, finding an article that’s actually positive about BYND, is like finding a pink diamond.

It seems like the WHOLE PLANET is negative towards BYND, yet the share price just keeps grinding upwards crazily, and despite coming down recently of late, still stays stubbornly high.

As I type this, the share price of BYND is USD 154.77.

I remembered punching in some numbers, scratching my head, and muttering that the world has gone crazy, that the numbers absolutely don’t make any sense………….. when the share price was at USD 100+.

This is as bubblish as my kids’ bath tub when they are left to their own devices.

I won’t illustrate why I think BYND is disgustingly over valued, even now. No investing thesis here. Cos everybody already knows the conclusion, why would I waste my time to illustrate it?

It has come down from the ridiculously high USD 220+, but it’s still dumb nevertheless.

Everybody knows it’s mad to do so, so who exactly is buying? If nobody’s buying, what’s keeping the share price elevated?

The answer lies in the low liquidty and float.

For the record, I agree with ALL the esteemed writers, talking about how BYND is an obvious short. Sure.

But because of the low float, the share price is kept high via a series of repeated short squeezes.

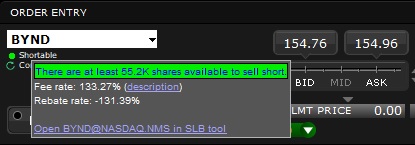

Borrowing costs for BYND is as crazy as it’s valuation:

And this is already a much better situation for borrowers. About a month or so ago, you couldn’t borrow any BYND shares to short AT ANY COST.

Zero.

The shares were the MOST EXPENSIVE to borrow in the entire US, across all exchanges.

This makes shorting BYND an extremely risky endeavor and 1 whereby the risk-benefit ratio is highly stacked against the shortists.

Upon every 1 tiny bit of positive news, the share price rockets up, and the sudden jump in the share price forces shortists to cover at an increasing price. The rush of buyers to cover at the elevated price, further causes the share price to spike up, and that brings in a new bunch of poor shortists who were forced to cover.

Now, I say they were FORCED to cover, cos it’s exactly that. They really were forced to.

For some, it’s simply cos they shorted on margin, and were squeezed out. For others, it’s cos the losses hit their risk limits, and they had to cut loss and cover their shorts.

But even if you weren’t in either scenario, even if you had all the capital in the world to back your short positions, even if you decided to stare down the world and short BYND till it’s grave… you couldn’t.

The lack of shares for borrowing means that you’d be forced to cover, regardless!

And that’s the sole reason for the bubble inflating and inflating and inflating.

Anyone talking about “business fundamentals”, or “revenue growth”, or “growth in market share” or “proprietary intellectual property” or whatever, is being naive..

It’s pure emotions, and a unique set of conditions resulting in a bubble that’s unseen for a long while.

Despite agreeing with all the short articles above, and the many more that I didn’t paste here, I gotta say that most, if not all, have been unprofitable. Most of those folks have lost money for the reason that I’ve described.

Having shorted earlier (and covered quickly), I was 1 of those folks above. The logical bunch. The rationale, data driven, intellectuals. The smart money, so to speak.

Yet, my BYND shorts were overall, loss making. (Note the past tense! :) )

Not anymore.

The tide has turned, and nett nett, my overall BYND shorts have finally, turned a profit.

Much of it is due to pure dumb luck, having shorted by selling naked calls at somewhere near it’s peak:

Implied volatility then was something like 90%, and the premiums were absolutely crazy to reflect the uncertainty just prior to ER.

On a side note, I’ve also made a ton coincidentally.

BYND announced a tie up with APRN, and that resulted in a single day jump in APRN’s shares of something like 15%.

I thought it was absolutely ridiculous and shorted APRN as a result, expecting to hold that for a couple of months until the fad dies off and/or the underwhelming numbers come in.

It took a couple of days instead. Literally a couple.

2 days:

So what’s next?

I’m still not borrowing any BYND shares to short. Borrowing costs are still crazy, and it just doesn’t make any sense to try to swim against the tide.

Even if one has high conviction that you’d beat the tide… we gotta rem that we have to swim against the tide… and STILL swim faster than our dear benchmark S&P. And as I’ve illustrated earlier, S&P is a damn fast swimmer!

In short, there’re just better and easier ways to make some money huh.

I’m currently short BYND, having sold a bunch of calls. All of the calls are expiring in 2 weeks, and I really don’t envision any of them getting exercised. If they are, I’d be covering them on the same day. No taking on a direct short position overnight….

until the lock up expiry.

You see, as part of BYND’s IPO, the insiders and major shareholders have their shares locked up for 6 months.

Supposedly anyway. BYND management and insiders “unlocked” this lock up and sold a bunch of shares themselves recently in a secondary offering. That’s something I’ve never seen personally, but anyway, that’s another story altogether.

The point here is, the insiders deem fit to take profit and let go of a chunk of their own shares at USD 160. I’m not sure why ANYONE would think it wise to buy shares above USD 160. Or even anywhere near there.

You’d have to be a super genius, or super idiot, to believe that you can value it more accurately than the founder and CEO and entire management team.

Anyhow, come the end of Oct, the lock up expires and I just don’t see how the major shareholders wouldn’t be keen and itching to sell out at least a portion, to lock in their profits at the current valuation.

Right now, they’re probably like race horses at the start of the race, just waiting for the race doors to open.

When that happens, liquidity would be restored, and the market can finally function normally again. Shortists would not be unfairly squeezed out, and the weighing machine can begin to weigh BYND for what it’s truly worth.

Until then, my plan is mainly to sell naked calls as and when, the premiums make it worthwhile. But because it’s impossible to hold a direct short position, or rather, there’s no way I want to be caught in that situation, so the only naked calls I’d be selling are far OTM ones.

I think the climate and opinion has changed with the secondary offering. Sure, you’d still get some resilience cos the float is still pretty low… but the number of dumb buyers just hoping on the train hoping for a quick buck, has pretty much thinned out.

Once liquidity is restored, we’d see who has the last laugh.

After October though, I might look to start piling into the puts, provided I get a good price for them. I don’t think it’d take too long for this to play out: I’m pretty sure the large institutional SHs are also pretty keen and raring to get some shares liquidated, having seen the insiders and management team sell some of theirs themselves. So I don’t think it’s necessary to get the LEAPS.

I like this pic.

It’s basically a summary of everything I wrote above:

Wrong. Buzz Lightyear.