My troubles started literally right after CNY, and since then, what can go wrong, has gone wrong, what cannot go wrong, has also gone wrong and what is already wrong, has gone more wrong.

Here are the numbers:

2024 (YTD):

SPY: +8.31%

VT: +6.37%

STI: -3.29%

TTF: -4.99%

SINCE INCEPTION (FEB 2020), ANNUALIZED:

SPY: +13.93%

VT: +10.25%

STI: -0.15%

TTF: +19.07%

Note: Returns are MWRs, all figures in USD

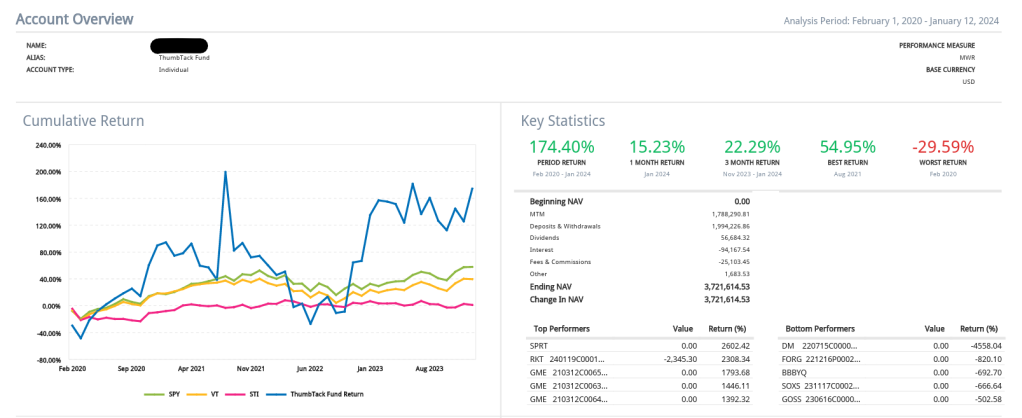

TTF’s NAV: USD 3,126,486.21

Deposits/Withdrawals: USD 2,053,609.26

Net capital gains since inception: USD 1,072,876.95

Since TTF was incorporated in Feb 2020, this means that TTF has enjoyed a net gain of USD 1,072,876.95 over a period of 48 months of investment activity, which works out to be USD 22,351.60 every month, or approximately SGD 29.8k per month from Feb 2020 to date.

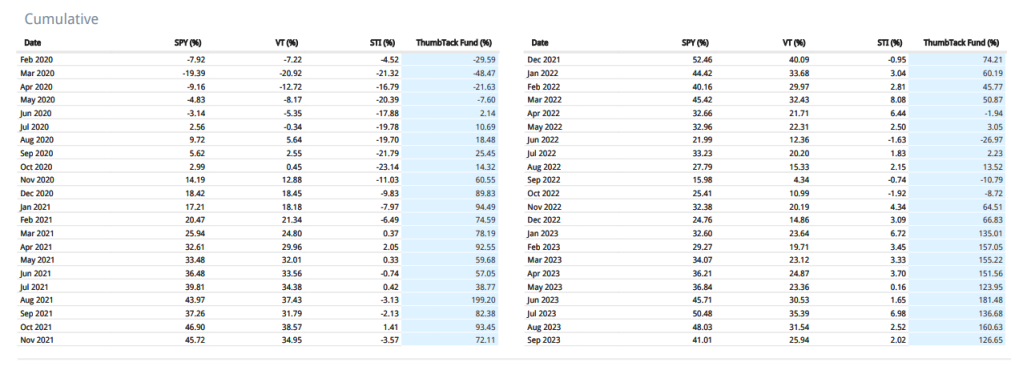

Cumulative ROI (Feb 2020 to Mar 2024):

SPY: +70.51%

VT: +49.08%

STI: -0.63%

TTF: +104.31%

TTF has generated double digit money weighted returns every year since inception:

Thus far, I’m able to write that “TTF has generated double digit money weighted returns every year since inception”.

Maybe I won’t get to write this after this year.

It’s an uphill task to turn this around, after a disastrous start. 1st quarter of 2024 is almost over, which means I have another 3 quarters to turn around a -5% YTD MWR and make it double digits. Tough.

So what went wrong?

Almost everything man.

But I’ve analyzed and recognized that most of the losses came from several short positions (which I shall not name), as well as a sizable long position in natural gas futures. And right this instant, natural gas is un-naturally unwanted.

Within the span of 1 month (since the last report), TTF’s AUM has dropped from about $3.7mil, to the current $3.1mil or so. That’s a huge $600k usd reversal in the span of 1 month! Damnit. I should’ve liquidated everything before CNY, and gone on a 1mth sabbatical leave and go travel into the far reaches of the planet, staying off the grid, and I’d now return to SG, 1 month later, and $600k usd richer.

It’s crazy.

And hmmm. Not very fun, to be honest.

But then again, neither am I hitting the panic button. Cos this isn’t my 1st rodeo. Not the 1st, won’t be the last time either.

Furthermore, when times were good, I’ve already mentally prepared that there’d be 1 such tough period coming up anytime. In fact, I’d be surprised if this didn’t come.

OK, I’m gg to bunker down and fight my way outta this rough patch.

Afterall, a $600k reversal is just merely 1x concentration into a really good idea, OR average positioning into 2 or 3 moderately good ideas. And historically, I’ve been able to get a least a couple of moderately sized ideas successfully.

I know title sounds like it’s click bait, but it’s not. Specifically, TTF AUM grew USD 492,647 in the 2 weeks since we started 2024, entirely from capital gains.

I wasn’t expecting to do an update so soon, but TTF really ploughed through some of the milestones that I thought would take many more months to accomplish. Mostly due to 2 concentrated moves that I made at the end of Dec 2023. More on that later…

2024 (YTD):

SPY: +0.29%

VT: -0.40%

STI: -1.50%

TTF: +15.23%

SINCE INCEPTION (FEB 2020), ANNUALIZED:

SPY: +12.28%

VT: +8.83%

STI: +0.30%

TTF: +29.19%

Note: Returns are MWRs, all figures in USD

TTF’s NAV: USD 3,721,614.53

Deposits/Withdrawals: USD 1,994,226.86

Net capital gains since inception: USD 1,727,387.67

Since TTF was incorporated in Feb 2020, this means that TTF has enjoyed a net gain of USD 1,727,387.67 over a period of 47 months of investment activity, which works out to be USD 36,752.92 every month, or approximately SGD 48.8k per month from Feb 2020 to date.

Cumulative ROI (Feb 2020 to Jan 2024):

SPY: +57.88%

VT: +39.59%

STI: +1.20%

TTF: +174.40%

TTF has generated double digit money weighted returns every year since inception:

And the results are amazingly wide. Like you wouldn’t expect some guy in the 2nd scenario, to underperform the 1st scenario by such a MASSIVE margin over 35 years. Can you imagine how the 2nd scenario guy feels in those +60% years? And he gets 1 of that every 5 years! He’d feel indestructible! And still he loses to the steady 20% compounder.

I wrote that way back in 2017, and it’s fast becoming my favorite post. I actually refer back to it myself from time to time. Therein, you can see how my thought processes form over the years. Hence, my focus on TTF being an all weather portfolio. I don’t want to lose money in any given year, whether it’s a bull or bear market. That post in 2017 highlights the basis for this.

Also, in the 1st scenario (steady 20% CAGR over 20 years), I posted this table:

Yr

Beginning Capital

Capital at Yr End

1

$1,000,000

1.2

$1,200,000

2

$1,200,000

1.2

$1,440,000

3

$1,440,000

1.2

$1,728,000

4

$1,728,000

1.2

$2,073,600

5

$2,073,600

1.2

$2,488,320

6

$2,488,320

1.2

$2,985,984

7

$2,985,984

1.2

$3,583,181

8

$3,583,181

1.2

$4,299,817

9

$4,299,817

1.2

$5,159,780

10

$5,159,780

1.2

$6,191,736

11

$6,191,736

1.2

$7,430,084

12

$7,430,084

1.2

$8,916,100

13

$8,916,100

1.2

$10,699,321

14

$10,699,321

1.2

$12,839,185

15

$12,839,185

1.2

$15,407,022

16

$15,407,022

1.2

$18,488,426

17

$18,488,426

1.2

$22,186,111

18

$22,186,111

1.2

$26,623,333

19

$26,623,333

1.2

$31,948,000

20

$31,948,000

1.2

$38,337,600

21

$38,337,600

1.2

$46,005,120

22

$46,005,120

1.2

$55,206,144

23

$55,206,144

1.2

$66,247,373

24

$66,247,373

1.2

$79,496,847

25

$79,496,847

1.2

$95,396,217

26

$95,396,217

1.2

$114,475,460

27

$114,475,460

1.2

$137,370,552

28

$137,370,552

1.2

$164,844,662

29

$164,844,662

1.2

$197,813,595

30

$197,813,595

1.2

$237,376,314

31

$237,376,314

1.2

$284,851,577

32

$284,851,577

1.2

$341,821,892

33

$341,821,892

1.2

$410,186,270

34

$410,186,270

1.2

$492,223,524

35

$492,223,524

1.2

$590,668,229

Since TTF is at the start of year 5, my target, according to this table, should be $2,073,600. But TTF is CAGR close to 30% currently, so I’m ahead of schedule by about 3 years currently… I’m more like at somewhere around year 8. So yeah, definitely still on track for $590mil! And hopefully before year 35! LOL.

I’d share the 2 positions leading to these gains and the thought process behind it, but before that, lemme just address 2 other points real quick.

In my last post, I wrote that SPY’s 2023 ROI is +26.19%. Someone wrote to me to ask if I made a mistake cos S&P was commonly quoted as having a +24% or so return in 2023. I’d just like to clarify that these numbers are calculated by InteractiveBrokers, and not by me, and I don’t think they’d make a mistake, cos otherwise, well, it’d just create mayhem for all the big funds using them.

The +24% figure refers to S&P’s return, the INDEX. Not the ETF. The ETF is SPY (or other similar ETFs), and it includes dividends. Since we cannot actually invest in an index directly, it doesn’t make sense to calculate your return and benchmark it against the index. It makes more sense to me, to benchmark against the ETF tracking the index, since it includes dividends. Basically, what I want to know, is how well or poorly I’m getting compensated for my activity vis a vis the passive ETF.

The 2nd point I’d like to talk about… and I hope I’m not being too intrusive here….. relates to yet another reader who asked me about shorting. Basically said reader told me that he got retrenched recently, is of a certain age so finding employment again is tough, and he was hoping to get some trading gains in order to cope with living expenses.

Oh boy.

Hand on heart, I really really really legit hope that as we get more retrenchments, not more people think like this. It’s extremely dangerous to think like this IMO. Trading like this, adds undue pressure, clouds your judgement, and just really, is not a wise activity to undertake. Might as well be trying to earn a living by going to the casino. The odds are just mightily stacked against you.

Regardless of how tough things may seem, trying to day trade randomly without a competitive advantage, in the hope that that’d be the cure for your problems is just…………. suicidal. It won’t solve your problems, but will magnify it greatly.

And to begin with, I don’t really day trade, so I’m not the best person to ask. But it just does not make sense to me.

Please don’t do it.

Alright, the bulk of the half a million in gains in the past 2 weeks comes from 1 long and 1 short position, both of which netted me 6 digits each in gains.

The long position was in Ambrx Biopharma (AMAM). Johnson & Johnson made an offer to acquire AMAM for $2bil, and overnight, I clocked in a 6 digit profit. The share price is up some ridiculous amount in 2024:

This is 1 of the competitive advantages that I’ve been trying to build for the past few years. Currently, I’d say that I can fairly accurately hunt down, and predict which are the pharma companies that’d likely get acquired AT SOME POINT.

The only problem is, I can’t tell exactly WHEN it’d take place. I can make some intelligent guesses, based on several factors. Let me explain.

Some background here for the uninitiated: the US biopharma space is without any doubt, the sector where the most M&A activity takes place. By far. The big boys look out for promising drugs to acquire. The smaller players, well, they actually NEED the big boys too, without whom, they probably can’t bring the drugs to market entirely by themselves.

The big boys don’t start acquiring any tom dick harry though, so forget about those companies at the start of the journey, with only Phase I or Phase II results/FDA approvals. It’d have to be closer to the end, minimally, starting from Phase III, when there is visibility to the end point.

Also, I find it easier to focus specifically on companies with a single drug in the pipeline. Companies with too many drug trials ongoing… it gets much harder to predict.

Finally, and most importantly, understanding the specific market and where the drug stands vis a vis it’s competitors, is probably the most important predictive factor. Is this a “best in class” drug? Would it be the drug of 1st choice for most clinicians in this situation? Stuff like that.

Now, most people think the situation is like this: we have a disease, and these drug companies do R&D, find some drug that’d treat the disease, do all the trials, and finally get FDA to approve it, and once it’s approved, they sell the drug, and the company makes a boatload of money.

That’s what happens in the movies. I can’t actually remember when was the last time I saw any pharma company get it so smooth sailing.

The reality is more like this: the pharma company spends a ton of money on a trial for a certain drug, turns out the results are… ok, not too bad, it does help the patient… BUT there are other better drugs out there already, and they seem to be performing BETTER.

What should the pharma company do? They already spent like a ton of money on this, they can’t just stop halfway. They have investors to answer to. Yet, what’s the point of throwing yet more money, and many more years of trials, only to come up with a drug which works, but doesn’t work as well as what is already existing in the market? Who the hell wants to take a 2nd best, new drug when there is already a better one? FDA won’t approve that, and even if FDA does, nobody is going to buy that 2nd best drug.

So they go peer into the results, stare hard at the numbers, and ah hah! They found that although the existing drugs have a better effect overall…. for a small subset of patients, the ones below a certain age, their drug seems to work better!

So they spend more money, do new trials with participants of that younger age group, and show to FDA that tadah! hey, our drug may not be as efficacious as the existing one, but for this particular age group, we are better! Here are the results!

So now, FDA says ok, fine, but your drug indications are narrowed ok? So your market size has reduced, so u can only tell drs that your drug is specifically for this age group only.

But oh wait, we also noticed that there are all these nasty side effects! Damn, I can’t approve this!

So the pharma company goes back yet again, looks at the data, and goes back to FDA and says… look guys, yes there are all these side effects, but we did new trials to show that the improvement in the treatment results is significant for this age group, and the side effects are……… rare and when they occur, they are… manageable, we just have to tweak the formulation, so instead of it being a liquid form, it’s now a pill form, cos the pill protects the GI system on the way down, so it’d only start acting in the stomach. So no more side effects ok? Stuff like that.

And finally, FDA says ok ok, I’d approve. But I gotta slap a black box warning on it ok, so that I don’t get into trouble. It literally looks like this:

In short, the actual process is actually very complicated, with big money pumped in, a lot at stake, all or none kinda situation, with lotsa twists and turns.

And in fact, to me at least, most of the time, it feels like it’s not about trying to find a medicine to treat a disease. The whole process feels more like “ok, great, now I have this medicine that does THIS. What disease can I treat it with?” Yup, medicines looking for a disease to treat.

But you see, I’m not FDA. I’m not here to judge the pharma industry. I’m here to make some serious money for TTF. So twists and turns are not only good, they are welcomed… if I can be ahead of the pack. And I think I actually can.

And why do I think I can? You know, I think every intelligent investor, has to really go through a multi year process of discovery and finding his own unique capabilities, coming up with his own style. Everybody knows WB, and by now, everybody can tell how he modified his value investing style from a cigar butt strategy, to a more focused approach on competitive advantage aka moats.

To cut a long story short, basically, Avenue Therapeutics (ATXI) was seeking FDA approval for IV Tramadol, something that I was familiar with.

While pouring over their submissions, I noticed a flaw in their study design, and that lead to results that I thought was not going to pass FDA. I even studied and found other comparable situations with another company (Recro Pharma) who submitted for a different drug (IV Meloxicam), and failed to get FDA approval, for the exact same reason as what ATXI did.

I wrote to then CEO Lucy Lu with my findings and concerns, showed her all the data that I’ve found and the other company as a comparison.

Maybe it’s cos I had built up a somewhat substantial shareholding in ATXI by then.

Maybe it’s cos my email was packed with supporting documents and data

Maybe it’s cos I actually made some sense and the email sounded like I knew what I was talking about

Maybe it’s simply cos I was a fellow dr too

In any case, Lucy Lu actually replied me promptly, and in the email, she actually cc-ed some of the board members of ATXI.

Unfortunately, the email replies did not really address my queries. She basically said the example I mentioned was not comparable (without explaining why), and basically said the key sticking point that I brought up (study data interval of pain score taking was too far apart, so the initial onset of analgesia at 30mins was too long, so their study did not support the use of IV Tramadol as a monotherapy), was not an issue cos it’s “faster” than what their data showed.

I brushed it off because I thought, well, surely the CEO and these board members (most of whom are also fellow drs), would know better. Her answer was vague, probably cos she can’t reveal market sensitive info to me on paper. Lucy Lu sounded damn confident, and at that time, I thought that well, I’m just a small fry here in SG, surely they’d know better than me. If she can give me a written reply stating her full confidence, hey, who am I to question these geniuses? It’s a US listed company for god’s sake! Better don’t keh kiang and make a fool outta myself.

…

…

…

CAN YOU IMAGINE HOW I FELT WHEN FDA REALLY REJECTED THE DRUG APPLICATION FOR THE EXACT SAME REASON THAT I WROTE TO LUCY LU ABOUT?!?!?!

Well, at that time, I was absolutely livid. Really a I-TOLD-YOU-SO moment.

I lost some money from ATXI, but I remember it was a manageable amount, cos just prior to FDA rejection, I cut loss on a portion of my stake.

On hindsight though, I’d credit this experience as a turning moment. Cos it made me realize, and I’m sorry to sound a bit arrogant here, but it really made me realize that I am onto something here. I can actually beat not just the average joe, not just the markets, hell, I can even beat the supposed geniuses and the supposed insiders!

They don’t always know more than me. For some of them, it’s just a damn job they go to, they go to work, they knock off at 5pm, and they’re looking forward to the weekend, or maybe they’re just following some schedule, some protocol that the parent company set, or whatever.

They can’t beat a determined TTI looking to grow his own hard earned money, peering through the data deep into the middle of the night. Nothing gives real motivation like putting your own money on the line.

So yes, that’s a turning point for me. And I might have lost some money as a result of the FDA rejection, but it’s money well spent.

If you’re interested, go see that post, and the few posts preceding it. I have it all documented. The fact that I can just type and explain everything off the top of my mind, already shows you how much of an impact this had on me.

On a different note… and I only just noticed this myself whilst writing this post, in that old post back in 2020, I wrote this:

hehe… good old days. I definitely front ran the crowd, since I build this position to number 2 BEFORE the mania started. (Think I wrote another post about it, but I also exited too early, think from the time I exited to the peak, I left another USD 21million on the table! Damnit, I wasn’t that experienced with bubbles then)

Alright, let me move on.

The 2nd position I had, was basically a direct short (plus some puts) on the bitcoin miners.

Now for some reason, crypto is machiam like a religion. People get all flustered and pissed when you are not on their side, for some weird reason that I’d never be able to comprehend. So all you crypto maniacs, don’t get your knickers/panties in a twist first, let me explain.

Sometime in Oct/Nov 2023, I started building LONG positions in some btc miners, specifically MARA and RIOT.

As the share price went ballistic, and we all know the reason why (BTC ETF approval), I got all my shares sold via call options that were assigned. I had a low 5 digit gain at this point.

I was happy with the reasonable gain, and would’ve been happy to sit this one out, except that the share price kept going up and up and up until it just felt absolutely ridiculous to me.

BTC ETFs aren’t some new innovation, neither are they bringing in some new product to the markets. For the meteoric rise to be justified, imo, it must have 2 factors: a new product that was previously unavailable, AND massive demand that was unfulfilled previously.

Well BTC ETFs doesn’t have either. It’s not a new product as in BTC isn’t new. Sure, you might have SOME increased demand because some folks might not want to hold BTC previously under some exchange, or even under their own cold wallet, but would suddenly trust some other institution to hold it…. but it’s not new. It’s not a situation whereby BTC didn’t exist yesterday, and suddenly, it’s listed and existed.

Institutional demand you say? Possible. Sure. But I’d just point out that Microstrategy was trading at a DISCOUNT to the value of the BTC they held prior to this. Markets try to be as efficient as they can, and that discount is already extremely telling to me.

The BTC ETF isn’t a productive ETF either. They aren’t producing some earnings, neither are they even trading the BTC to generate profits. It’s literally just HOLDING BTC. It’s no different from you holding onto BTC on your own. So the product IS THE SAME. Only the entity holding it is different.

It doesn’t fulfill the 2nd criteria either. You possibly might have more demand for the reasons I mentioned, but it’s not a massive demand cos anyone who wanted BTC, could’ve bought it. You don’t have a long queue of people just dying for the ETF to be listed so that they could buy it. It’s not Taylor Swift concert tickets.

You see, if there was a free market for Taylor Swift concert tickets, the prices would’ve gone absolutely ballistic, and I wouldn’t have dared to short it!

Cos there is a NEW product. The tickets wouldn’t have existed before Taylor Swift announced her tour.

And there’s no way for fans to get their hands on the tickets until they came on sale. It’s not like there have always been tickets flying out there for the past 3 decades, and anyone could’ve bought it.

So yes, TS tickets (assuming no rules against re-selling) would not have been a bubble imo. I might’ve sneered and laughed at those fighting for it… but no, I wouldn’t have shorted TS tickets.

Which can only mean that the ballistic share price of these btc miners is driven by people buying simply cos they expect other people to be buying!

Even then, by itself, I don’t think it’s a shorting opportunity. Without a clear catalyst, more and more people can buy, and like Soro’s theory of reflexivity, the actions of some people crystallizes the changes in the markets, and that attracts other buyers and all that, setting off a positive feedback loop.

However, in this case, there IS a catalyst for a short position. The markets were viewing BTC ETF approval like it’s some holy grail. I was waiting in anticipation for it for the exact opposite reason. It’d be the catalyst that I needed.

I even wrote about this on InvestingNote before the approval, albeit, not very strongly or enthusiastically cos well, btc is a religion and you don’t go f around too much with religious fanatics, otherwise you’d end up like the Americanos. (hey hey, leave me alone ok, I was actually long MARA and RIOT ok! I was 1 of you guys! We are family!)

So as the share price kept climbing, all whilst I was gallivanting in the arctic circle, I took a break from making snowmen and started building a short position in Dec 2023. At first, I swung to the short side in MARA and RIOT since I was familiar with them, but added more shorts on HUT later on. Most of the short position was in the form of direct shorting, but I also bought some puts along the way, with the money I made from the long side.

There. Not kidding. This was the exact moment I started shorting:

Cos I had to wait for them and I had nothing else to do.

And I think very well in the cold.

MARA is down like 19%++ YTD:

RIOT is down 12% YTD:

HUT is down 16% YTD:

OK, that’s all the sharing I have in this post.

If I don’t write anything before CNY, here’s wishing everyone reading this a happy, fulfilling, huat Year of the Dragon ahead!